Free Consultation

(314) 500-HURT100+ years of combined experience and over $200 million won for our clients in Missouri and Illinois. Contact a personal injury lawyer near you.

Free Consultation

(314) 500-HURTOne evening in mid-June 2022, one of our clients, Colbert, was driving home, when another driver, moving at a high

rate of speed, was turning into a gas station and drove into Colbert’s lane. Colbert was transported to the hospital

by ambulance with substantial injuries.

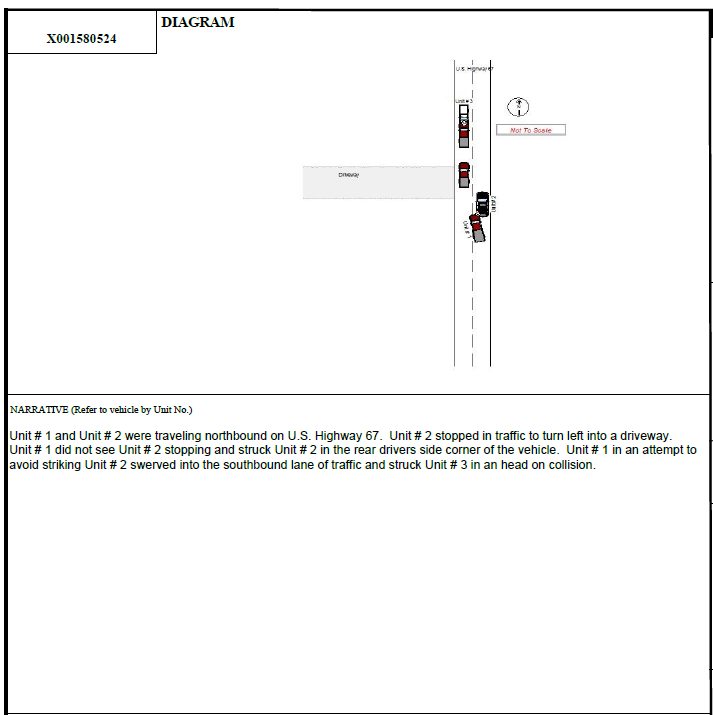

Although the police report showed that the accident was clearly the other driver’s fault (red car in the

diagram from the police report; hitting Colbert’s green car), as is frequently the case, the driver that hit

him had no automobile insurance.

Other times, someone is in an accident caused by a driver who has this “minimum” coverage, but that coverage

(e.g., $25K in Missouri) is less than the medical and other damages caused by the accident. These drivers

are called “underinsured motorist” (vs. “uninsured motorist” for those with no insurance).

When Colbert hired Burger Law, the only thing he knew was that the driver who hit him provided “no proof of

insurance” to the police officer.

Although consulting an attorney when in a vehicle accident is always wise, it is especially so when you have

to navigate what to do when the other driver is uninsured or underinsured.

To begin with, we have the tools to determine if the person really has insurance. And we can determine what coverage

they have.

And if they don’t have insurance, as was the case with the person who hit Colbert, Burger Law can seek compensation

from the client’s insurance. Specifically, when people purchase automobile insurance, they often wisely purchase

what is called “UM” or “uninsured” and “UIM” or “underinsured” motorist insurance.

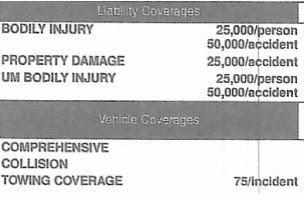

Thankfully, Colbert’s policy did include “UM Bodily Injury” coverage. This coverage is made precisely for the

situation he found himself in this accident. This insurance pays for his “bodily injury” damages when the

at-fault driver has no insurance.

People often think that because such insurance payments would come from their own insurance company, and not

the other driver’s company, they will not have any problems getting payment.

coverage, insurance companies often resist fully compensating their customers when they need to use it. Just like

at-fault driver insurance companies, they may offer just a fraction of damages sustained.

They will likely require documentation of the medical bills and not suggest their customers seek recovery for future

medical care that might be necessary or wage loss, or emotional distress damages, or pain and suffering. Insurance

companies are businesses and every dollar they pay out (including to their own customers) is lost profit.

After Colbert’s primary medical treatment was done (by October 2022), we drafted a comprehensive “demand letter” to

his insurance company which laid out his real damages including medical bills and lost wages and asked for payment

of “full policy limits” of $25K.

That letter went out in November 2022, and in December 2022 (almost six months to the day after accident), Colbert’s

insurance company offered him the full $25K.

Some cases take longer to settle and some cases don’t settle at all and need to be litigated. Regardless of what path

a particular case takes, having an attorney, like those at Burger Law, to navigate this process is critically

important to get you the compensation you deserve.

Founder | Injury Attorney

Gary Burger has dedicated his career to standing up against bullies. The founder and principal attorney of Burger Law | St. Louis Personal Injury Lawyer has helped hundreds of Missouri and Illinois individuals and families recover th …

Years of experience: 30 years

Location: St. Louis, MO

NO FEES UNTIL WE WIN YOUR CASE

We offer free consultations and are available 24/7 to take your call. Live chat, text, and virtual meetings are available.

or call us at